eaSi-system - Framework for systematic SDG impacts assessment

Offshore wind

Scenarios

- An expected 10-fold increase of offshore wind: Current (2020) global capacity is about 28GW and plans are to add more than 200 GW during the next decade, almost half of it in Europe, 40% in Asia and Oceania, and the remaining 10% in North America. There are also large untapped potentials in Latin America and the Caribbean as well as in Africa. The scenarios for offshore wind power in this study consider public intentions, strategies, and roadmaps from governments as a medium scenario, and are aligned with estimated scenarios from IRENA, windEurope, IEA and country-specific information.

- Upscaling potential in certain regions: China, the UK, the US, Germany, and the Netherlands would account for 60% of all installed offshore wind capacity by 2030. The global South has very high potential, despite of few policies and pledges. Electricity production from offshore wind in 2030 would be over 990 TWh. This electricity would have been enough to supply 272 million households, that is all of Europe, with electricity in 2020.

Changing value chains

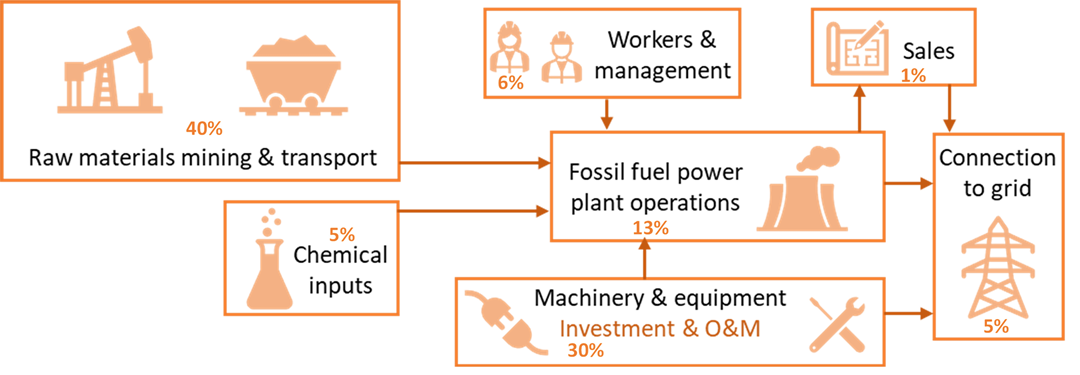

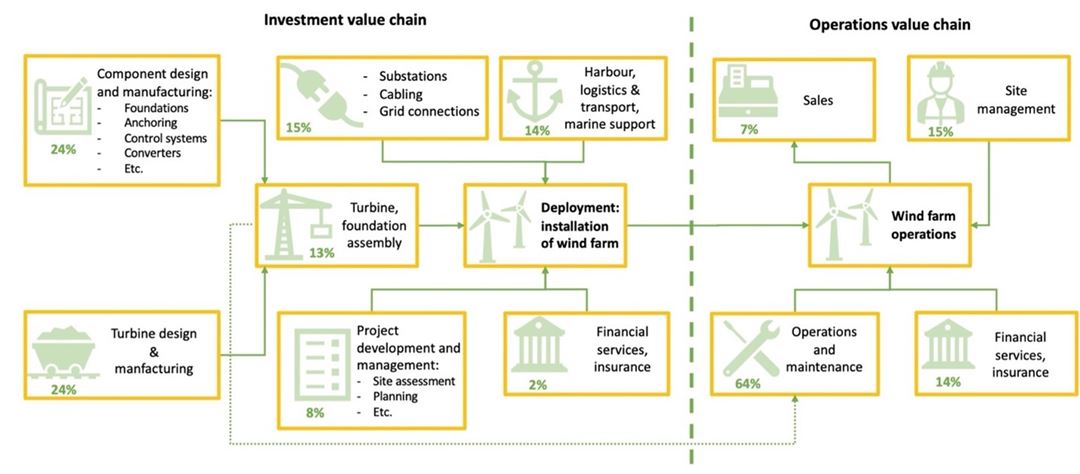

- Coal, gas and oil supply chains are replaced…

-

... By offshore wind supply chains

Offshore wind requires higher up-front costs than fossil fuel power plants for the technology itself as well as infrastructure investments such as

- new high-voltage cables

- new power stations

- new/adapted substations

However, the operation expenses of offshore wind are lower than those of fossil sources where fuel constitutes around 80% of production costs.

This impacts the Sustainable Development Goals (SDGs)

Across the world

For the offshore wind case, apart from the value chain effect identified in the model, we also identified several direct, indirect and interlinked effects on the SDGs. These effects are summarized in the figure below.